By Eric Flickinger, CPA, ABV | Manager, Business Valuation

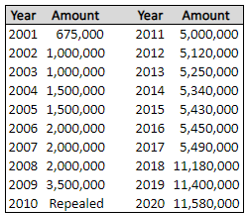

The Unified Tax Credit represents the amount of assets that an individual is allowed to gift to other parties without having to pay gift, estate, or generation-skipping transfer taxes. This credit is significant as amounts above this level will be taxed at rates starting at 18% and gradually increasing to 40% (as of 2020), based on the size of the estate. The unified tax credit has changed over the years, sometimes materially with each tax bill passed. However, over the past 20 years, the Unified Tax Credit has trended higher regardless of political party in control. The below table shows how the individual credit has changed over the past 20 years.

Several major tax law changes have created jumps in the unified credit over this period. The first was the Economic Growth and Tax Relief Reconciliation Act of 2001 (the “Act”) that was signed into law by President Georg W. Bush. This set the table for the unified tax credit to grow from $675,000 in 2001 through 2010 at which point, the Act fully repealed the estate tax. The Act was set to sunset in 2011, but instead the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 was signed by President Barack Obama, which temporarily set the credit at $5 million. The American Taxpayer Relief Act of 2012 set this level on a permanent basis. Then, the Tax Cuts and Jobs Act of 2017 was signed by President Donald Trump, which significantly increased the unified tax credit to $11.18 million with a sunset provision for 2025.

What to Prepare Going Forward

Election years bring a lot of uncertainty, especially involving tax laws. Clearly, with a Donald Trump victory, the expectation is that no change will happen to the current law. However, if Joe Biden wins and the Democrats take control of Congress, the tax law will once again be revisited. The Democrats would look to take apart the Tax Cuts and Jobs Act. This could mean returning the unified credit back to similar levels as when Joe Biden was Vice President or in the $5 million range. Further, Joe Biden has proposed eliminating the step-up in basis on inherited capital assets. If you are holding significant unrealized gains, the tax could be significant which you were previously planning on being able to avoid.

Planning Opportunities

If Joe Biden wins the election, estate tax planning will become very important for those who can take advantage of the historically high unified tax credit. One way to lock in the higher unified tax credit is to gift assets while the credit is higher. This technique will allow you to avoid paying any tax on assets up to $11.58 million (double that if you are married). Additionally, any appreciation in the assets after the gift will also avoid any taxation as the assets are out of your estate. With the step-up in basis at death potentially going away, you should consider revisiting your estate plan if you have a significant amount of unrealized gains. Without the step-up, you may want to look to look at optimizing your holdings and look at ways to potentially maximize the higher unified tax credit and/or take advantage of lower capital gains tax rates.